Filed pursuant to Rule 424(b)(4)

Registration No. 333-259740

PROSPECTUS

17,650,000 Shares

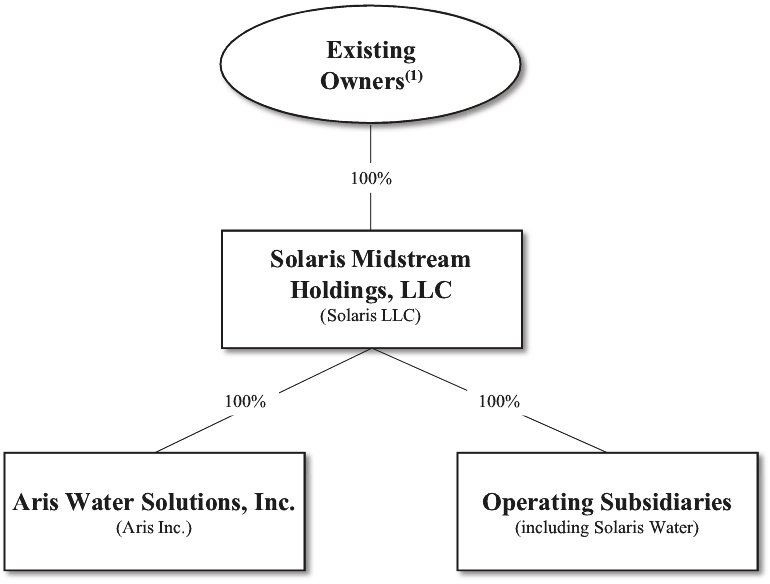

Aris Water Solutions, Inc.

Class A Common Stock

This is the initial public offering of the Class A common stock of Aris Water Solutions, Inc., a Delaware corporation. We are offering 17,650,000 shares of our Class A common stock.

Currently, no public market exists for our Class A common stock. We have been approved to list our Class A common stock on the New York Stock Exchange under the symbol “ARIS.”

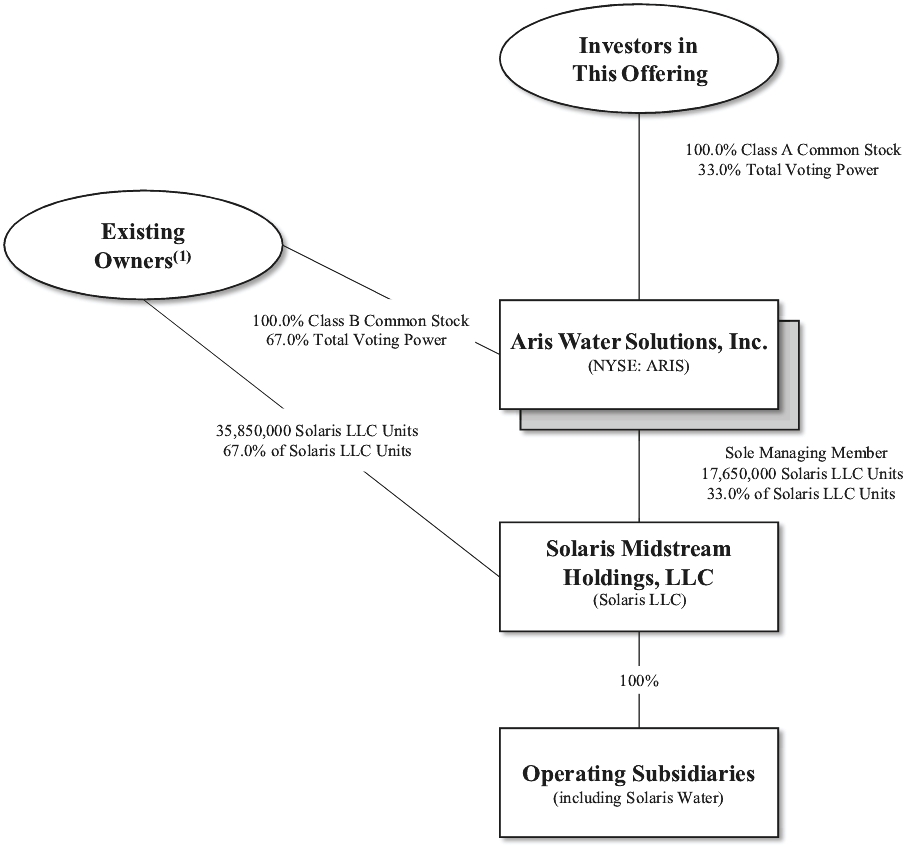

Each share of Class A common stock will entitle its holder to one vote on all matters to be voted on by stockholders generally. Each share of Class B common stock has no economic rights but will entitle its holder to one vote on all matters to be voted on by stockholders generally. Class A stockholders and Class B stockholders will vote together as a single class on all matters presented to our stockholders for their vote or approval, except as otherwise required by applicable law or by our amended and restated certificate of incorporation. Through their ownership of all the Class B common stock, our Existing Owners (as defined herein) will own 67.0% of the combined voting power of our common stock immediately after this offering. See “Corporate Reorganization.”

We are an “emerging growth company” as defined under the U.S. federal securities laws and, as such, have elected to comply with certain reduced public company reporting requirements for this and future filings. See “Risk Factors” and “Prospectus Summary—Implications of Being an Emerging Growth Company.”

Investing in our Class A common stock involves risks that are described in the “Risk Factors” section beginning on page 28 of this prospectus.

| | | Per Share | | | Total | |

Initial public offering price | | | $13.00 | | | $229,450,000 |

Underwriting discounts and commissions(1) | | | $0.78 | | | $13,767,000 |

Proceeds, before expenses, to us | | | $12.22 | | | $215,683,000 |

(1) | See “Underwriting” for a description of all underwriting compensation payable in connection with this offering. |

At our request, the underwriters have reserved for sale, at the initial public offering price, up to 5% of the shares of our Class A common stock offered by this prospectus (excluding the shares of Class A common stock that may be issued upon the underwriters' exercise of their option to purchase additional shares) to individuals, including our officers, directors and employees, as well as friends and family members of our officers and directors. For more information regarding the directed share program, please read “Underwriting—Directed Share Program.”

The underwriters may also exercise an option to purchase up to an additional 2,647,500 shares of our Class A common stock from us, at the public offering price, less the underwriting discount, for 30 days after the date of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The shares of Class A common stock will be ready for delivery on or about October 26, 2021.

Book-Running Managers

Goldman Sachs & Co. LLC | | | Citigroup |

J.P. Morgan | | | Wells Fargo Securities |

Barclays | | | Evercore ISI |

Co-Managers

Capital One Securities | | | Johnson Rice & Company L.L.C. | | | Raymond James |

| | | | ||||

Stifel | | | | | U.S. Capital Advisors |

Prospectus Dated October 21, 2021.